In banking, the chatbot conversation is no longer experimental. About 37% of the U.S. population interacted with a bank chatbot in 2022, and chatbots are projected to deliver $8 billion in annual cost savings for financial institutions, or roughly $0.70 per interaction according to the CFPB's research on chatbots in consumer finance. That changes the executive question. It's no longer “should we have a bot?” It's “what kind of banking interface are we building, and what risks are we willing to own?”

Most banks still treat conversational AI as a deflection layer. That's too small a vision. A serious AI chatbot for banking should authenticate safely, access the right systems, complete approved actions, confirm outcomes, and know when to escalate. It should fit into a broader operating model that includes channels, agents, workflow orchestration, data governance, and digital account servicing. For leaders modernizing adjacent infrastructure, this overview of digital banking solutions for CEFs is useful context because the chatbot only succeeds when it sits on top of sound digital rails.

The practical shift is from scripted assistants to autonomous service agents. Banks evaluating platforms for this next phase often start with industry-specific stacks such as AI agents for BFSI, but the more important issue is architectural discipline. If the agent can't complete a card freeze, dispute intake, payment flow, or onboarding step with controls and auditability, it won't move the needle where it matters.

Table of Contents

- The New Reality of Digital Banking

- From Answering Questions to Completing Tasks

- Inside the Engine of a Modern Banking AI

- Building a Fortress of Trust and Compliance

- Your Phased Implementation and Change Management Roadmap

- A Practical Checklist for Vendor Selection

- Measuring What Matters KPIs ROI and the Future

The New Reality of Digital Banking

Banking leaders don't need another reminder that customers want convenience. They need to recognize that conversational interfaces are becoming part of the bank's operating core. The customer no longer distinguishes between app navigation, assisted service, and chat. They see one bank. If the chatbot is weak, the brand feels fragmented.

That matters because the technology generation has changed. The first wave of banking bots was mostly keyword matching, decision trees, and FAQ routing. Those systems helped with low-risk, repetitive requests, but they rarely handled ambiguity well. Customers learned to work around them, not with them.

What's different now is the rise of agentic systems that can understand intent, pull account context, and trigger approved workflows. The strategic implication is straightforward. The AI chatbot for banking is moving from a peripheral service widget to a primary digital service layer.

Banking leaders should rethink the business case

The business case is broader than labor savings. A modern banking agent can reduce friction in servicing, shorten time to resolution, improve digital adoption, and preserve human staff for advisory and exception handling. Those benefits compound when the same agent works across chat, mobile app, web, and voice.

Three changes usually separate mature programs from stalled ones:

- They design for workflows, not answers. Customers want outcomes completed in session.

- They connect AI to bank systems. A smart front end without systems access becomes another dead end.

- They govern escalation aggressively. Sensitive moments still need people.

Practical rule: If your chatbot can explain a card freeze but can't complete one safely, customers will still view the experience as broken.

The strategic shift is already underway

The operational center of gravity is moving toward autonomous service. That doesn't mean removing humans. It means letting AI absorb predictable work and route exceptions with more context than legacy IVRs or static forms ever could.

Banks that win here won't merely deploy a chatbot. They'll build an orchestrated service layer that can act, explain, document, and hand off cleanly.

From Answering Questions to Completing Tasks

The fastest way to misunderstand an AI chatbot for banking is to think of it as a better FAQ engine. FAQ deflection is useful, but it isn't where durable value comes from. The bigger opportunity is task completion inside a controlled conversation.

Why FAQ bots fail in banking

Customers don't wake up wanting answers. They want progress. They want to move money, unblock a card, challenge a charge, update details, or finish onboarding. A bot that only replies with policy text creates one more step instead of removing one.

Research on financial inclusion makes the point clearly. Customers want chatbots to integrate financial data, support payments, and provide confirmations of completed actions, not just answer generic questions, as noted in Commonwealth's financial AI and chatbot guide.

That's the dividing line between a novelty and a service channel.

What task completion looks like in practice

A modern banking agent should handle work in layers.

First comes contextual service:

- Balance and transaction help: The agent understands which account the customer means and retrieves the right view.

- Card and account servicing: It can explain fees, due dates, holds, and recent activity in plain language.

- Product guidance: It can recommend next steps based on customer profile, eligibility logic, and approved content.

Then comes transactional execution:

- Payments and transfers: The customer initiates a payment, validates details, and receives confirmation in chat.

- Card controls: The agent can freeze or unfreeze a card through approved controls.

- Dispute intake: The bot gathers required details, structures the case, and confirms submission.

- Onboarding flows: It guides the user through document capture, identity steps, and application status checks.

The final layer is closed-loop confirmation. Many banks still fail in this aspect. After an action, the agent should confirm what happened, what the next status is, and what the customer should expect next. Without that confirmation, customers don't trust the transaction.

A conversational interface earns trust when it can both act and prove that it acted.

The design pattern that works

In practice, the strongest flows follow a simple pattern:

- Clarify intent in natural language.

- Authenticate at the right level for the requested action.

- Execute through approved system APIs or workflow tools.

- Confirm the result with an auditable message.

- Escalate when confidence or policy requires it.

What doesn't work is a pseudo-agent that pretends to be autonomous, then dumps the customer into a form or queue. That creates false confidence and usually increases frustration.

Banks should also be careful not to over-automate emotionally charged or regulated moments. A lost card freeze is often ideal for automation. A potential fraud narrative involving distress or vulnerability may need a human much earlier.

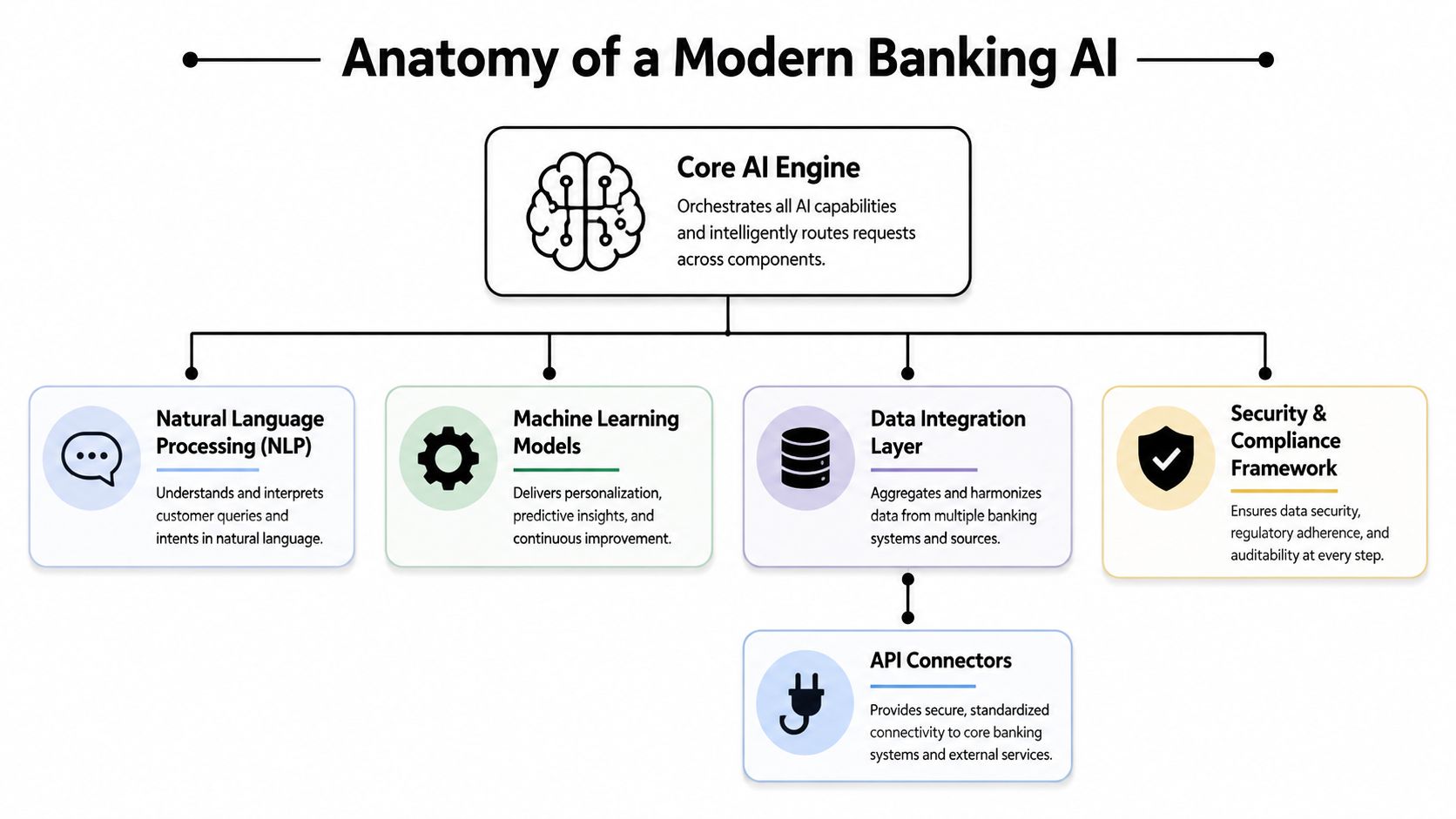

Inside the Engine of a Modern Banking AI

A modern banking agent looks simple from the outside. On the inside, it's an orchestration problem. Reliable performance doesn't come from one model. It comes from a stack that interprets requests, chooses the right reasoning path, retrieves trusted data, applies guardrails, and executes actions through bank systems.

Near the top of the stack, teams need a builder layer that lets them define flows, policies, prompts, integrations, and tests without turning every change into a long engineering cycle. That's where tools such as an AI agent builder fit into the delivery model.

The core stack behind reliable banking conversations

Think of the architecture like a high-performance engine. Every component has a specific job, and weak parts show up quickly under load.

Natural language processing is the intake system. It identifies intent, extracts entities, and interprets phrasing variants such as “lock my debit card,” “my card is missing,” or “pause card use.”

Large language models are the reasoning layer. In enterprise banking, one model usually isn't enough. Different tasks require different strengths. Fast routing tasks, summarization, policy explanation, and multi-step reasoning don't always belong on the same model path.

Retrieval-augmented generation keeps responses grounded. Instead of relying only on model memory, the agent pulls from trusted policies, product rules, knowledge repositories, and sometimes live banking data before it answers.

Integration services and APIs are the execution layer. This is what lets the bot do work instead of just talk about work. Without integration to core banking, payments, CRM, identity, fraud, and case systems, the experience stops at advice.

Policy and security controls sit across the stack. They decide what can be answered, what can be acted on, what needs masking, and what must escalate.

A useful explainer on how these layers come together in practice is below.

Why data quality is the hidden differentiator

Most failed banking bots are not language failures first. They are data failures. The model may interpret the request correctly, then pull the wrong profile attribute, an outdated fee rule, or an incomplete transaction record.

PwC notes that banks are using AI to automate data cleansing, enrichment, and classification, and that matters directly for conversational performance because better data improves intent recognition and personalized responses, while weak data hygiene creates inconsistency and operational risk in banking interactions, as described in PwC's analysis of how AI is reshaping banking.

For CIOs, that has two implications:

- Conversation quality is a data program. Treat customer, product, and transaction data as model inputs, not back-office exhaust.

- RAG does not fix bad source systems. It only surfaces them faster.

The architecture choices that age well

Banks should prefer architectures that reduce lock-in and let them evolve model strategy over time. That usually means:

- Model flexibility: The ability to route tasks across different model types.

- Composable integrations: APIs and middleware, not brittle custom point connections.

- Auditable retrieval: Clear visibility into what source informed an answer.

- Testable guardrails: Controlled prompts, confidence thresholds, and fallback logic.

The cleanest implementations don't chase novelty. They optimize for explainability, maintainability, and safe execution.

Building a Fortress of Trust and Compliance

Banking customers will tolerate a bot that is occasionally terse. They won't tolerate one that mishandles sensitive data, improvises a misleading answer, or traps them in a loop during a high-stakes issue. Trust is the hard currency here.

Trust is an operating design choice

A compliant banking agent starts with boundaries. It should know which intents are informational, which are transactional, which require step-up authentication, and which should never be automated end to end. That sounds obvious, but many teams still design from the front end backward. They start with the conversation and only later ask what policy permits.

The better pattern is to start with control points:

- Authentication policy: Match identity assurance to the requested action.

- Data handling: Minimize exposure, mask sensitive data, and log access.

- Auditability: Record what the customer asked, what the AI did, and why.

- Action gating: Restrict execution to approved workflows and role permissions.

Banks modernizing payment-related service flows should also align bot design with current security requirements such as PCI-DSS v4.0.1 compliance guidance, especially when the agent participates in payment or card-related interactions.

Compliance should shape the user journey early. If it arrives at the end as a review function, the redesign work will be expensive.

Where safe escalation matters most

A bank should not optimize for maximum containment. That's a contact center metric mindset, not a trust mindset.

Bridgeforce recommends tracking safe escalation and wrong-answer complaints to reduce risks such as UDAAP, and also notes that the highest-value strategy is precise containment plus reliable escalation for sensitive cases in financial services, as outlined in its guidance on monitoring AI chatbot effectiveness in banking.

That principle matters in several edge cases:

- Vulnerable customers: Low literacy, confusion, dependency, or possible financial abuse indicators.

- Emotional distress: Fraud fear, bereavement, hardship, or urgent access problems.

- Regulated ambiguity: Disputes, complaints, adverse decisions, and policy-sensitive requests.

- Language complexity: Multilingual interactions where nuance affects the outcome.

The controls that build customer confidence

The strongest banking programs make trust visible to the customer. They don't hide behind AI fluency.

Consider adding these design behaviors:

- Explicit confirmations: Tell the customer what action was completed and what remains pending.

- Clear boundaries: Say when the agent can't decide or shouldn't decide.

- Seamless handoff: Pass history, identity state, and structured context to the human agent.

- Consistent disclosure: Make it clear when the customer is interacting with AI.

That last point matters more than many teams assume. Customers don't object to automation nearly as much as they object to uncertainty.

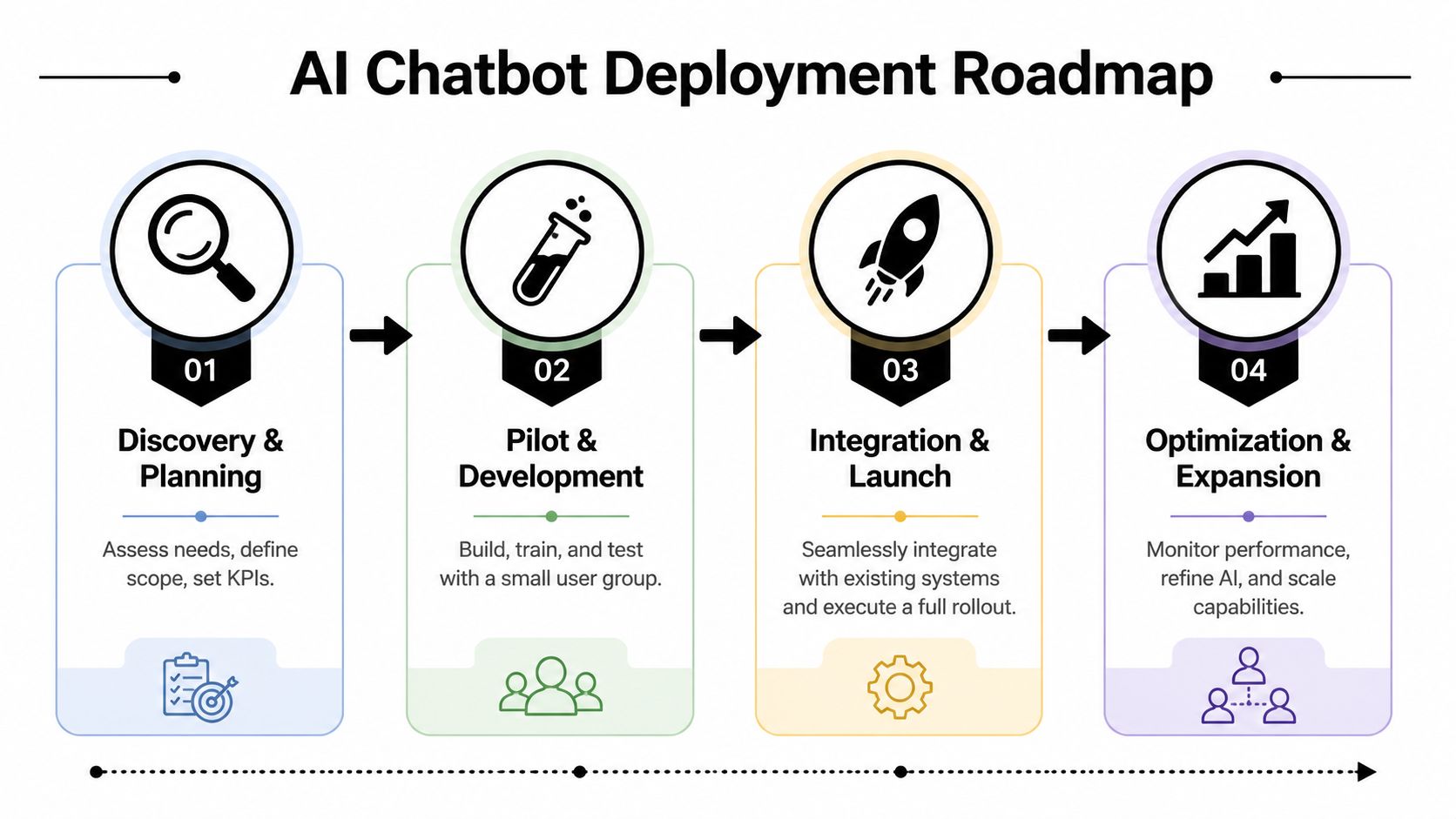

Your Phased Implementation and Change Management Roadmap

The biggest mistake I see in banking AI programs is trying to launch a polished, enterprise-wide assistant too early. Banks should build an operating muscle, not a demo. The roadmap needs to be phased enough to reduce risk, but ambitious enough to create momentum.

Phase one starts smaller than most banks expect

A good pilot is narrow, measurable, and operationally real. Don't begin with “all retail banking support.” Start with a handful of journeys where policy is stable and value is easy to observe.

Strong pilot candidates often include:

- Card servicing basics: Freeze or unfreeze flows, status checks, replacement requests.

- Routine account servicing: Balance explanations, recent transaction help, branchless service needs.

- Internal employee support: Banker and agent assistance before customer-facing expansion.

The key is to pick workflows where the bank can prove control, not just response quality.

Integration and testing decide the outcome

Once the pilot proves customer language patterns and basic routing, the heavy work begins. This is the point where many vendors overpromise and bank teams underestimate integration complexity.

Focus on three workstreams in parallel:

System integration

Connect the chatbot to identity, core banking, CRM, knowledge systems, and case tools through governed APIs. Avoid brittle shortcuts that bypass enterprise standards.Conversation and workflow testing

Test real language, not ideal prompts. Include vague phrasing, incomplete requests, interruptions, code-switching, and frustrated users. Banks should simulate edge cases relentlessly.Control validation

Confirm that masking, escalation, transcript logging, and fallback behavior work as designed under real traffic conditions.

A practical implementation habit is to define “failure-ready” behavior before rollout. Decide what the bot should do when data is missing, APIs time out, user identity is uncertain, or policy confidence drops.

The best banking bots are designed as much for uncertainty as for success paths.

Change management is not a side workstream

Many banking AI programs hit technical readiness before organizational readiness. Agents worry about job displacement. Risk teams worry about unseen exposure. Product owners worry that AI will distort customer journeys they already manage.

Banks need to address that directly.

A durable change plan usually includes:

- Agent role redesign: Position human staff around exceptions, advice, retention, and vulnerable-customer handling.

- Training on collaboration: Teach agents how to review AI context, correct outputs, and continue the conversation without repetition.

- Operational governance: Create a cross-functional group with CX, operations, IT, risk, compliance, and service owners.

- Internal communications: Explain what the AI does, what it doesn't do, and how success will be measured.

The best human response to AI in banking isn't resistance. It's specialization. As AI absorbs repetitive interactions, human agents can spend more time where empathy, negotiation, and judgment matter.

Rollout should be segmented, not big bang

Expand in rings. Start with a limited customer segment, channel, or journey family. Watch behavior closely. Then widen scope.

A practical rollout sequence often looks like this:

- Controlled release: Limited users, low-risk intents, strong monitoring.

- Broader servicing: More channels and more authenticated tasks.

- Transactional expansion: Payments, disputes, onboarding steps, and proactive service moments.

- Optimization loop: Update prompts, policies, retrieval sources, and escalation rules continuously.

Banks that rush past this sequence usually create rework for themselves. Quiet, disciplined expansion wins.

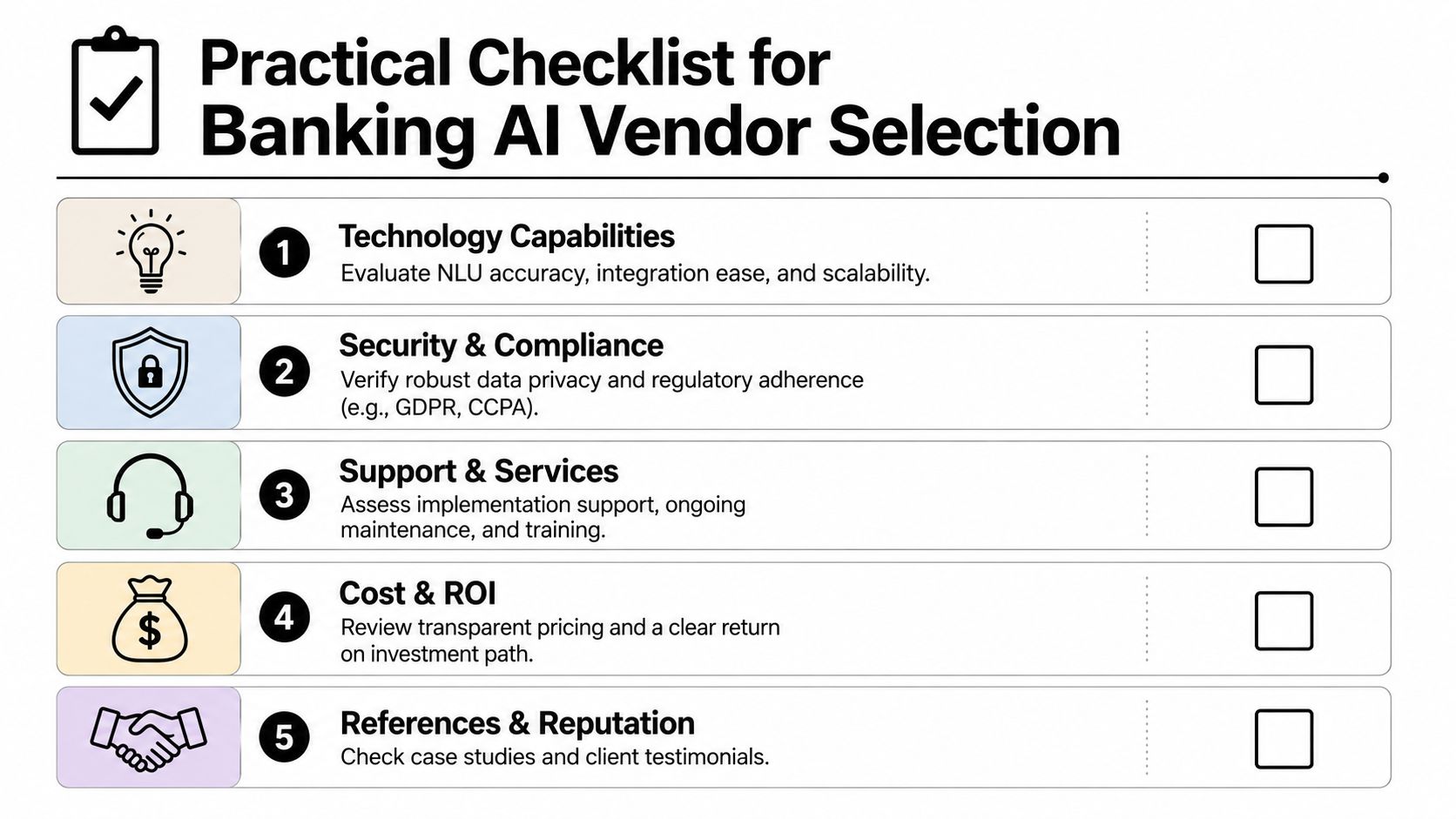

A Practical Checklist for Vendor Selection

Most banking AI purchases fail before implementation starts. The problem is not feature comparison. It's evaluation discipline. Banks buy a conversation layer when they should be buying an execution, control, and operating platform.

Questions that expose platform depth

The right vendor discussion starts with uncomfortable questions. Ask them early.

- Can the platform execute approved banking actions, or only answer questions? This separates workflow tools from knowledge bots.

- How does it handle retrieval and grounding? You need control over what sources the model can use.

- What does escalation carry forward? If the human agent loses context, the customer pays the price.

- How are policies enforced? Guardrails should be configurable, testable, and visible.

- What integration pattern is standard? Look for mature APIs, connectors, and orchestration options.

- How portable is the model strategy? Multi-model flexibility matters if pricing, latency, or risk posture changes.

One option banks may evaluate is Yellow.ai, which provides an enterprise AI platform with multi-LLM support, omnichannel orchestration, agent-building tools, and pre-built integrations. It's one of several categories of platforms that can fit banking programs, depending on architecture and governance requirements.

A workable evaluation table

Use a scoring model that forces teams to compare what matters for regulated service delivery, not just demo quality.

| Evaluation Category | Criterion | Why It Matters for Banking |

|---|---|---|

| Technology Capabilities | Supports transactional workflows | The agent must complete approved actions, not only provide answers |

| Technology Capabilities | Retrieval and knowledge grounding | Banking responses need traceable, trusted source material |

| Technology Capabilities | Omnichannel support | Customers move across app, web, voice, and messaging without changing expectations |

| Technology Capabilities | Integration depth | Core banking, CRM, identity, fraud, and case systems must connect reliably |

| Technology Capabilities | Model flexibility | Banks need room to adapt model strategy for cost, latency, and control |

| Security and Compliance | Audit trails | Every automated action and response should be reviewable |

| Security and Compliance | Data handling controls | Sensitive customer and payment data must be protected throughout the interaction |

| Security and Compliance | Role-based governance | Different teams need controlled access to prompts, flows, and analytics |

| Security and Compliance | Escalation controls | The platform should support policy-driven handoff for risky or sensitive cases |

| Services and Support | Implementation support | Banking launches depend on orchestration across multiple teams and systems |

| Services and Support | Testing and optimization tools | Teams need to validate flows before release and improve them after launch |

| Commercial Fit | Pricing clarity | Banks need to understand how cost changes with usage, channels, and model mix |

| Commercial Fit | Roadmap alignment | The vendor should support where the bank is going, not just where it is today |

What to watch for in demos

Demos are often polished in exactly the wrong places. Be skeptical of:

- Perfect prompts: Real customers don't speak in curated sample utterances.

- Thin integrations: A screen mockup is not workflow completion.

- Vague compliance answers: If the vendor cannot explain auditability clearly, the gap is real.

- One-size-fits-all AI claims: Banking requires configurable control, not generic intelligence.

A practical procurement process includes IT, service operations, risk, compliance, and frontline owners in the same room. If only innovation or only procurement runs the process, blind spots appear quickly.

Measuring What Matters KPIs ROI and the Future

A banking chatbot program should be judged the way any serious service operation is judged. Did it improve customer experience, reduce friction, contain costs responsibly, and expand service capacity without increasing risk?

The KPI set should reflect that.

Start with three KPI groups

Customer experience

Track satisfaction, complaint themes, handoff quality, and whether customers had to repeat themselves after escalation.

Operational performance

Measure containment with caution, not as a vanity target. More useful metrics are successful task completion, escalation quality, first-contact resolution, and how often the AI routed the customer correctly on the first pass.

Financial impact

Watch cost per inquiry, staffing mix, and service volume absorbed digitally.

The performance delta between old and new systems is material. Traditional rule-based banking bots show a 29% customer satisfaction score, while modern conversational AI platforms reach 72%. Modern systems can handle 80% to 90% of routine inquiries and cut the cost of a single inquiry by 50%, according to Galileo's analysis of why banking chatbots have low customer satisfaction rates.

ROI should be calculated conservatively

The right ROI model starts with a narrow set of use cases and values outcomes you can defend. Count handled inquiries, reduced manual effort, lower repeat contacts, and service hours shifted to higher-value work. Then subtract integration, governance, maintenance, and change management costs.

What matters most is quality-adjusted automation. A bank that automates more volume but creates more complaints hasn't improved the business. It has only moved work downstream.

The future is autonomous, but controlled

The future of the AI chatbot for banking is not a chattier assistant. It's an autonomous service agent that can complete more financial workflows safely, across channels, with better judgment about when not to act.

That future belongs to banks that combine ambition with control. Autonomous banking will not be built by prompt engineering alone. It will be built by disciplined architecture, clean data, clear guardrails, and service design that customers can trust.

If you're evaluating how to build an AI chatbot for banking that goes beyond FAQs into secure, auditable task completion, Yellow.ai is worth a look. Its platform supports agent building, omnichannel orchestration, and enterprise controls that banking teams typically need when moving from simple automation to autonomous service.